The National Agency on Corruption Prevention (NACP) continues to audit declarations submitted for the 2022-2024 reporting periods, during which, among other things, it investigates the acquisition of assets by declarants and their family members at prices significantly below market value. This mainly concerns the purchase of vehicles.

NACP analysed data from the public section of the Register of Declarations on the number of vehicles declared at potentially undervalued prices:

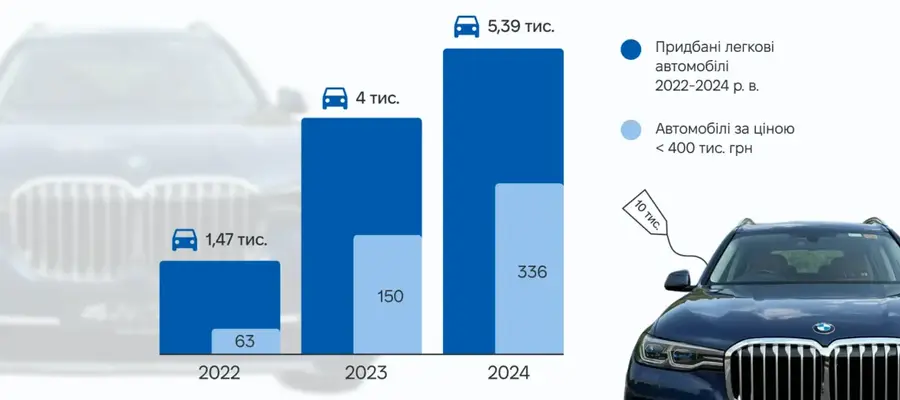

- in 2022, declarants acquired 1,470 passenger cars manufactured in 2022, including 63 at a price of less than UAH 400,000;

- in 2023, the number of passenger cars manufactured in 2022 and 2023 purchased amounted to 4,000, including 150 at a price of less than UAH 400,000;

- in 2024, 5.39 thousand passenger cars manufactured in 2022-2024 were purchased, including 336 at a price of less than UAH 400 thousand.

During full audits of declarations, NACP repeatedly recorded cases where declarants or members of their families acquired vehicles at prices significantly lower than the average market price. Does this always indicate a violation?

The cost of a car is primarily influenced by its wear and tear (most often these are cars purchased at auctions abroad) and/or technical condition (as a rule, these are cars after accidents that require significant repairs). Therefore, it is important for declarants to keep documents confirming the circumstances under which the vehicle was purchased at a price lower than the market price.

The formation of a car price significantly lower than the market price may also be influenced by family ties between the seller and the buyer (for example, an agreement between brothers, spouses, etc.).

On the other hand, the purchase of a car from third parties without objective reasons for underestimating the market price may indicate:

- a hidden gift or even an unlawful benefit;

- a reduction in the tax base and, as a result, the amount of payments to the budget;

- an unjustified asset, i.e. concealment of the amount of actual expenses due to the buyer's inability to confirm the source of the funds.

It should be noted that in the event of the discovery of unjustified assets, NACP will focus on the market value of the asset, rather than the valuation made at the time of acquisition (Part 3 of Article 290 of the Code of Civil Procedure of Ukraine).

For example, a member of the Obukhiv City Council included in her 2023 declaration information that a member of her family had purchased a 2018 MERCEDES-BENZ S 560 for UAH 149,000 and a 2017 TOYOTA CAMRY for UAH 10,000. During a full audit of the declaration, it was established that the market value of these vehicles was over UAH 2.9 million and UAH 717,000, respectively. At the same time, the income of the declarant and her family member from confirmed sources did not allow for such expenses. During the audit, inaccuracies in the valuation of the declared assets and signs of unjustified assets were identified. NACP forwarded the relevant materials to the Specialised Anti-Corruption Prosecutor's Office for consideration of the issue of filing a lawsuit to confiscate the assets for the state.

In some cases, in order to conceal the value of an asset by significantly underestimating it, declarants select ‘Not applicable’, “Unknown” or ‘Family member did not provide information’ in the declaration field for the value.

For example, the secretary of a district court in the Odesa region selected ‘Not applicable’ in her 2023 declaration regarding the value of a 2017 BMW X3 and a 2005 MERCEDES-BENZ SPRINTER 213 CDI she acquired during the reporting period. According to the purchase agreements, the cars were purchased for UAH 50,000 and UAH 10,000, respectively, which is 95-98% lower than the market price for such vehicles. At the same time, the market value of such cars is over UAH 987,000 and UAH 326,000, respectively.

The audit also found that the actual income received by the declarant and her husband from official sources did not allow them to incur expenses in the amount of the market value of the cars, taking into account other expenses in the reporting year. Based on the audit findings, the National Police of Ukraine is conducting a pre-trial investigation.

Concealing the real value of cars is most often associated with possible attempts to evade taxation. NACP reports such cases to the State Tax Service of Ukraine.

In October 2024, the Resolution of the Cabinet of Ministers of Ukraine was adopted, which improves the procedure for commission trade in vehicles.

In particular, for the purchase and sale of vehicles, it is now mandatory to submit a document confirming the value of the vehicle. The implementation of this mechanism is expected to increase state budget revenues, ensure a fairer approach to trade in vehicles, and reduce the number of cars declared at undervalued prices. For more details, please click here.

Note: in accordance with Article 62 of the Constitution of Ukraine, a person is presumed innocent of a crime and cannot be subjected to criminal punishment until their guilt has been proven in accordance with the law and established by a court verdict.

More results of full audits and relevant reports can be found in the section “Results of NACP activities”.